A mortgage loan is a type of loan specifically designed to help individuals purchase real estate, typically a home. It is one of the most common financial instruments used by buyers who do not have the full amount of money required to pay for the property upfront. Mortgage loans are secured by the property itself, meaning the lender has a legal claim on the home until the loan is fully repaid.

Key Takeaways:

- A mortgage loan helps individuals buy property by borrowing money secured by the home.

- The borrower repays the loan with interest over a set term.

- Failure to repay may result in foreclosure.

- Understanding types, terms, and eligibility is crucial for making informed decisions.

What is the Definition of a Mortgage Loan?

Understanding the Mortgage Loan Concept

A mortgage loan is a legally binding agreement between a borrower and a lender. The lender provides a sum of money to the borrower to purchase real estate. In return, the borrower agrees to pay back the loan amount plus interest over a specific period, often ranging from 15 to 30 years. The real estate property serves as collateral. If the borrower fails to meet the repayment terms, the lender can take ownership of the property through a process called foreclosure.

How Does a Mortgage Loan Work?

The Basic Mechanism

When you apply for a mortgage loan, the lender assesses your financial situation, creditworthiness, and the value of the property you want to buy. Upon approval, you receive the loan amount, which you use to pay the seller. You then make monthly payments to the lender, which cover both the principal (the amount borrowed) and the interest (the cost of borrowing). Over time, as you pay down the principal, you build equity in the property.

Components of a Mortgage Payment

- Principal: The original loan amount.

- Interest: The fee charged by the lender for lending money.

- Taxes: Property taxes collected by the lender on behalf of the local government.

- Insurance: Homeowners insurance, which protects against damage or loss.

What Are the Different Types of Mortgage Loans?

Fixed-Rate Mortgage

A fixed-rate mortgage offers a consistent interest rate and monthly payments throughout the loan term. This predictability helps borrowers budget effectively.

Adjustable-Rate Mortgage (ARM)

An ARM has an interest rate that changes periodically based on market conditions. Initial rates are often lower than fixed rates but can increase or decrease after a set period.

FHA Loans

Backed by the Federal Housing Administration, FHA loans cater to first-time homebuyers or those with lower credit scores. They typically require smaller down payments.

VA Loans

Available to veterans and military personnel, VA loans offer favorable terms, including no down payment and competitive interest rates.

Jumbo Loans

For loan amounts exceeding conforming limits, jumbo loans provide financing but often come with higher interest rates and stricter credit requirements.

How to Qualify for a Mortgage Loan?

Eligibility Criteria

Lenders evaluate several factors before approving a mortgage loan:

- Credit Score: Higher scores increase approval chances and better interest rates.

- Income and Employment: Stable and sufficient income reassures lenders of repayment ability.

- Debt-to-Income Ratio (DTI): Lenders prefer a DTI below 43%.

- Down Payment: Typically 3-20% of the property price, depending on the loan type.

- Property Appraisal: Confirms the home’s market value matches the loan amount.

Documentation Required

- Proof of income (pay stubs, tax returns)

- Credit history report

- Bank statements

- Identification documents

What Are the Advantages and Disadvantages of Mortgage Loans?

Advantages

- Homeownership: Enables individuals to buy homes without paying the full price upfront.

- Equity Building: Monthly payments build ownership in the property.

- Tax Benefits: Interest payments may be tax-deductible.

- Predictable Payments: Fixed-rate loans offer financial stability.

Disadvantages

- Long-Term Debt: Mortgage loans span many years, affecting financial flexibility.

- Risk of Foreclosure: Missing payments can lead to losing your home.

- Interest Costs: Over time, interest can add up to a significant expense.

- Upfront Costs: Closing costs and down payments require significant initial funds.

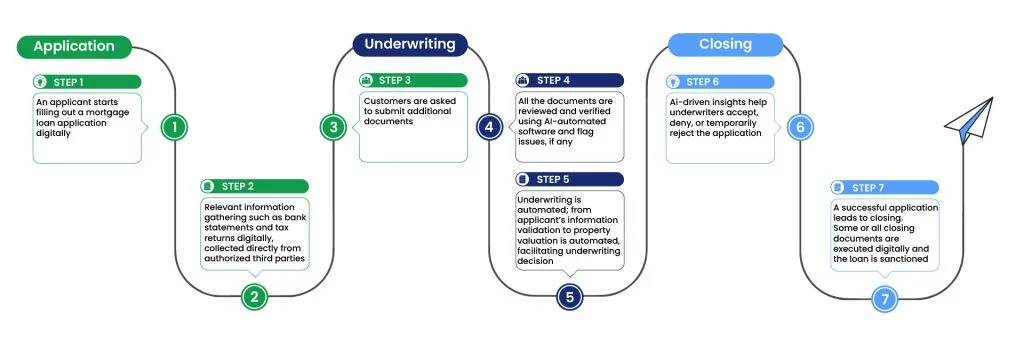

What is the Mortgage Loan Application Process?

Step 1: Pre-Approval

Before house hunting, borrowers often get pre-approved by a lender. This step assesses how much you can borrow and your loan eligibility.

Step 2: House Shopping and Loan Application

After pre-approval, you find a home and formally apply for the mortgage loan.

Step 3: Loan Processing and Underwriting

The lender verifies all information, reviews your financials, and orders a home appraisal.

Step 4: Loan Approval and Closing

Once approved, you sign the loan documents and pay closing costs. The property title is transferred to you, and the loan officially begins.

What Are Common Terms Used in Mortgage Loans?

- Amortization: The process of spreading out loan payments over time.

- Principal Balance: The remaining loan amount yet to be repaid.

- Escrow Account: Holds funds for taxes and insurance.

- Points: Fees paid upfront to reduce interest rates.

- Closing Costs: Fees paid at loan finalization, including legal and administrative costs.

How Can You Manage Your Mortgage Loan Effectively?

Tips for Successful Mortgage Management

- Make Payments on Time: Avoid penalties and maintain good credit.

- Consider Refinancing: When interest rates drop, refinancing can reduce payments.

- Make Extra Payments: Reduces principal faster and saves on interest.

- Keep Emergency Funds: Protects you during financial hardships.

What Happens if You Default on a Mortgage Loan?

Understanding Foreclosure

If payments are missed for several months, the lender may start foreclosure proceedings to repossess and sell the property. Foreclosure severely damages credit scores and makes obtaining future loans difficult.

Alternatives to Foreclosure

- Loan Modification: Adjusting loan terms for affordability.

- Short Sale: Selling the home for less than owed with lender approval.

- Deed in Lieu of Foreclosure: Voluntarily giving the property back to the lender.

What Is a Mortgage Loan?

A mortgage loan is a type of loan specifically designed to finance the purchase of real estate, most commonly a home. Unlike unsecured loans, mortgage loans are secured by the property being purchased, meaning that the lender can repossess the property through foreclosure if the borrower fails to meet repayment obligations. Mortgage loans typically involve a large principal amount that is repaid over a long period, such as 15, 20, or 30 years. These loans come with interest, which is the cost charged by the lender for borrowing the money. The borrower’s monthly payments usually include principal, interest, taxes, and insurance. Mortgages are a fundamental financial product in the real estate market, making homeownership accessible to millions who would otherwise be unable to afford a home outright.

Types of Mortgage Loans Explained

Mortgage loans come in various forms tailored to different borrower needs and financial situations. The most common types include fixed-rate mortgages, where the interest rate and monthly payments remain the same throughout the loan term, providing stability and predictability. Adjustable-rate mortgages (ARMs) start with a lower fixed rate but can change based on market conditions, which can lead to fluctuating monthly payments. Government-backed loans, such as FHA, VA, and USDA loans, offer benefits like lower down payments and more flexible qualification requirements, making them ideal for first-time buyers or those with less-than-perfect credit. Jumbo loans, designed for high-value properties exceeding conventional loan limits, usually require stricter credit profiles and larger down payments. Understanding these options is key to selecting the right mortgage that fits your financial situation.

How to Qualify for a Mortgage Loan?

Qualifying for a mortgage involves demonstrating your ability to repay the loan. Lenders evaluate your credit score, income stability, employment history, and debt-to-income (DTI) ratio. Typically, a credit score of 620 or higher is required for conventional loans, although government-backed loans may allow lower scores. Income verification includes pay stubs, tax returns, and bank statements. Lenders prefer a DTI ratio below 43%, meaning your monthly debt payments should not exceed 43% of your gross monthly income. The size of your down payment also plays a role; larger down payments can improve your chances of approval and secure better interest rates. A property appraisal is also conducted to ensure the home’s value justifies the loan amount. Meeting these criteria is essential to getting a mortgage approved.

Fixed-Rate vs. Adjustable-Rate Mortgages: Which Is Better?

Choosing between a fixed-rate and adjustable-rate mortgage depends on your financial goals and risk tolerance. Fixed-rate mortgages offer a consistent interest rate and payment schedule, which means your monthly payment remains the same for the entire loan term. This stability makes budgeting easier and protects against interest rate increases. In contrast, adjustable-rate mortgages start with a lower introductory rate but can adjust periodically based on market interest rates, potentially lowering your payments initially but also increasing them later. ARMs are suitable for borrowers who plan to sell or refinance before the adjustment period or who anticipate rising incomes. Understanding these differences helps borrowers pick a mortgage that aligns with their long-term financial plans.

The Mortgage Loan Application Process: Step-by-Step

Applying for a mortgage involves several stages, each requiring careful preparation and attention to detail. First, borrowers often get pre-approved to understand their borrowing limits, which involves submitting basic financial information to lenders. After pre-approval, you find a home and formally apply for the mortgage. Lenders then verify your income, credit history, and assets, and order a property appraisal to confirm its market value. The underwriting process assesses all information to determine if the loan meets the lender’s criteria. Upon approval, you receive a loan commitment letter. The final step is closing, where you sign the loan documents, pay closing costs, and receive the keys to your new home. Understanding each step helps avoid delays and surprises.

Understanding Mortgage Interest Rates

Mortgage interest rates are the cost you pay to borrow money from the lender, expressed as a percentage of the loan principal. These rates fluctuate based on broader economic factors such as inflation, the federal reserve’s policies, and the housing market’s supply and demand. Your personal credit profile, loan type, and down payment size also influence the interest rate offered. Lower interest rates mean lower monthly payments and less paid in interest over the life of the loan. Borrowers can choose between fixed rates, which stay the same, or adjustable rates, which can change periodically. Monitoring market conditions and maintaining good credit can help you secure favorable interest rates.

What Is Mortgage Refinancing and When Should You Consider It?

Mortgage refinancing involves replacing your existing mortgage with a new loan, usually to obtain better terms such as a lower interest rate, reduced monthly payments, or a shorter loan term. Refinancing can save you significant money over time but comes with closing costs and fees. Homeowners often refinance when interest rates drop substantially or if their credit improves. Another reason to refinance is to switch from an adjustable-rate mortgage to a fixed-rate loan for payment stability. Cash-out refinancing allows borrowers to tap into their home equity for major expenses like home improvements or debt consolidation. It’s important to weigh the costs against potential savings to decide if refinancing makes financial sense.

What Happens During Foreclosure?

Foreclosure occurs when a borrower fails to make mortgage payments as agreed, and the lender takes legal action to repossess the property. The foreclosure process varies by state but generally begins after several missed payments. The lender sends notices of default, and if payments are not made, the property is auctioned to recover the owed loan amount. Foreclosure has serious consequences, including damaging the borrower’s credit score and making it difficult to secure future loans. However, borrowers may avoid foreclosure through loan modifications, repayment plans, short sales, or deed in lieu of foreclosure, which allow them to negotiate with lenders to prevent losing their home.

How Does Property Appraisal Affect Your Mortgage Loan?

A property appraisal is a professional assessment of a home’s market value, conducted by a licensed appraiser during the mortgage process. Lenders use the appraisal to ensure the loan amount does not exceed the home’s worth, protecting their investment. If the appraisal value comes in lower than the purchase price, buyers may need to negotiate a lower price, increase their down payment, or risk loan denial. Accurate appraisals ensure that borrowers do not overpay and lenders do not lend beyond the property’s value. The appraisal affects loan approval, terms, and sometimes the interest rate.

Benefits and Risks of Government-Backed Mortgage Loans

Government-backed loans, such as FHA, VA, and USDA loans, provide accessible Financing options with lower credit score requirements, smaller down payments, and flexible terms. FHA loans help first-time buyers with limited savings, while VA loans offer no-down-payment mortgages to eligible veterans and active military members. USDA loans support rural property purchases with zero down payment. These programs reduce barriers to homeownership but often require mortgage insurance premiums or funding fees that increase overall costs. Understanding the benefits and potential costs helps borrowers decide if government-backed loans align with their financial needs.

Also Read : What Is a Home Loan and How Can You Benefit from It?

Conclusion

A mortgage loan is a powerful financial tool that enables millions to achieve the dream of homeownership. Understanding how mortgage loans work, the different types available, and how to qualify is crucial for making informed decisions. While mortgage loans come with long-term financial commitments and risks, effective management and careful planning can maximize their benefits. Whether you are a first-time buyer or looking to refinance, educating yourself on the intricacies of mortgage loans will help you navigate the real estate market confidently.

FAQs

1. What is the minimum down payment for a mortgage loan?

The minimum down payment varies by loan type. Conventional loans typically require 5-20%, FHA loans can require as low as 3.5%, and VA loans may require no down payment.

2. How is the interest rate on a mortgage loan determined?

Interest rates depend on factors like credit score, loan type, loan amount, market conditions, and lender policies.

3. Can I pay off my mortgage early without penalty?

Many loans allow prepayment without penalties, but some have prepayment fees. Check your loan terms before making extra payments.

4. What is mortgage refinancing?

Refinancing means replacing your existing mortgage with a new loan, usually to get a lower interest rate or change loan terms.

5. How long does the mortgage approval process take?

Typically, 30 to 45 days, depending on documentation completeness and lender efficiency.

6. What happens if I miss a mortgage payment?

You may incur late fees, and after several missed payments, the lender can start foreclosure proceedings.

7. Can I get a mortgage loan with bad credit?

It’s possible but challenging. FHA loans or specialized lenders may offer options with higher interest rates and stricter terms.